The outlook for China A-share market following its recent strong rally

July 07, 2020 | Author: David Chao, (Global Market Strategist)

China A-shares have staged a strong +32% rebound since the lows in March and around 15% in the last week and remain my favorite asset class. Although I am cautious about sentiment driven rallies and I wouldn’t be chasing the market, I think that the recent outperformance continues to have legs for the rest of the year because of 4 key reasons below.

Strong Economic Recovery

It’s becoming more apparent that Chinese fundamentals are improving and that its very likely that China will be one of the few countries in the world to experience a solid V-shaped economic recovery and eek out positive GDP growth this year. Daily indicators such as property sales, coal use and traffic congestion along with a host of other high-frequency data points across various industries – point to the world’s second largest economy operating at full or near-full capacity compared to the levels at the end of 2019. The proof is in the economic data, the most recent industrial profits growth of +6.0% in May as well as the June PMI sequential improvement to 50.9 and the Caixin services PMI hitting 58.4, a 10-year high. These trends confirm that corporate earnings should be positive in 2020 and that the economy is well on its way to stage a strong comeback.

Mitigated COVID-19 Resurgence Risk

Chinese policymakers have been able to quickly squash the additional waves of new COVID-19 infections since March, the most recent being the 344 cases found in Beijing. What’s important to note, is that each new wave of infection has been met with more and more precise testing and quarantine measures that do not require broad lockdowns that sacrifice economic growth. Countrywide daily infections have been under 20 in June, underscoring the country’s ability to successfully contain the pandemic. This has allowed the government to ease commercial restrictions, as measured by the economic stringency index by Oxford University’s Blavatnik School of Government.

Compelling Valuation

China is in a much more progressed economic recovery stage and pandemic containment when compared to its other peers, yet the onshore equity market trades at a 40% P/E discount to the S&P 5001. This is the highest valuation divergence since April 2014. That being said, when compared to historical valuations, Chinese stocks appear somewhat expensive, trading around 13.x P/E versus a 5-year average of 12.1x although if we adjust for the pandemic and look at earnings on a 24-month basis, valuations are more reasonable, currently at 11.9x vs a 5-year average of 11.0x1.

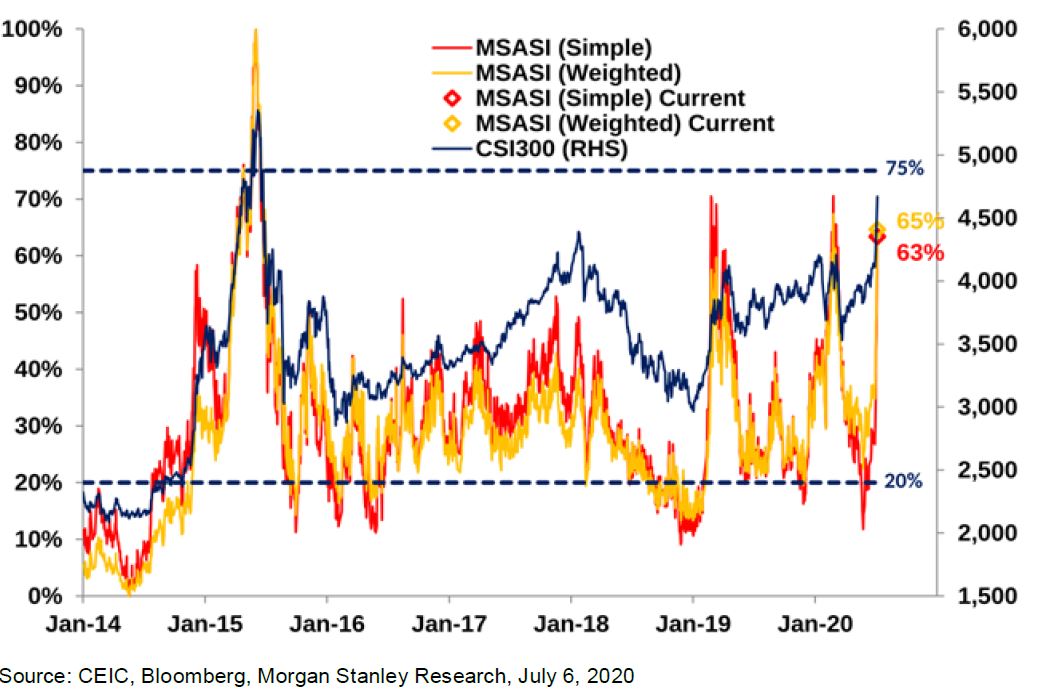

Improving Retail Sentiment

The chart below shows that China A share sentiment has improved significantly to 65%, with a 13% jump in one trading day. This is the 3rd largest daily jump since 2014, following the 25th February 2019 (improving US-China trade relations) and 4 Feb 2020 (COVID-19 correction rally). In the past, only a reading of over 75% would indicate that the regulators would look to impose cool-down measures. In addition, improving retail sentiment has driven up the stock market’s turnover velocity and margin financing.

Although I’m wary of retail investors speculating on the stock market, and I think there could be a bit of that here, I’m not overly concerned yet for a key reason. When compared to the 2015 A-share rally, margin financing, particularly the OTC margin financing, accounted for around 10% of the free float market cap2. Currently, margin financing only comprises of around 4% of the free float market cap2 – although I’m sure that is going to increase and I am keeping a close eye on this data point.

Morgan Stanley A-Share Sentiment Indicator

Conclusion

In the end, I argue that in the long run, improving economic fundamentals will ultimately sustain risk asset performance compared to tremendous but diminishing returns of loose monetary policies. Key risks remain, such as a resurgence in COVID-19 new infections in the US and other EM countries that will sap demand of Chinese goods as well as geopolitical risks such as a flare-up in US-China relations.

I think that market participants are starting to see through the shrill rhetoric from both sides and starting to realize that there is limited economic impact from the war of words. What bears watching is whether the worsening bilateral relations will lead to further technology and financial decoupling between the two economies. Already we’re seeing concrete export control actions taken against certain Chinese technology companies, and initial congressional actions taken to delist Chinese companies in the US. In the meanwhile, I think that investors will focus back on the basics: economic fundamentals. It’s very black and white to me where fundamentals are improving and that’s where investors should be putting their money to work.

1 Source: Bloomberg, as of July 7, 2020

2 Source: Morgan Stanley, as of July 7, 2020